What are you looking for:

News and publications

The fuel and energy complex (FEC) finds itself in a state of heightened turbulence on Wednesday, August 12, 2026. The oil market is once again held hostage by geopolitics: Brent prices exceeded $90 per barrel for the first time since late July after negotiations between the USA and Iran regarding the full opening of the Hormuz Strait hit a deadlock. The European gas market sends alarming signals — underground gas storage (UGS) is only filled to 59%, significantly below the multi-year average ahead of the heating season. OPEC+ is concluding its cycle of increasing oil production quotas, electricity prices in Europe are rising despite a record share of renewable energy sources (RES), and the Russian oil products market remains under strict regulation: the ban on gasoline exports has been extended until the end of January 2027. Below is a detailed overview of key events in the oil and gas and energy sectors for investors and commodity market participants.

Current news on startups and venture investments as of August 12, 2026: Anthropic's preparation for the largest IPO of the year, mega funds and record concentration of venture capital, billion-dollar rounds in AI infrastructure and energy, a boom in defense technologies, and a revival in the exit market.

The fuel and energy complex (FEC) meets Tuesday, August 11, 2026, in a state of high turbulence. The main theme of the global oil and gas market is the protracted negotiations surrounding the unlocking of the Strait of Hormuz: Tehran claims to be in the final stage of coordinating shipping routes with Oman, yet imposes tough conditions on Washington, including the lifting of sanctions and payment of reparations. Against this backdrop, Brent oil has risen above $85 per barrel for the first time since early August, recovering part of the recent decline. Meanwhile, the European gas market is preparing for the most challenging winter in recent years: underground gas storage facilities (UGSF) are only 58% full — the lowest level in 15 years of observations. OPEC+ completes its cycle of production recovery, the Russian oil products market operates under a prolonged export ban, and the global electricity sector is restructuring under explosive demand from data centers and artificial intelligence. Below is a detailed overview of key events for investors, participants in the FEC market, and oil, gas, and fuel companies.<br /><br />

Current news on startups and venture capital investments as of August 11, 2026: a record $510 billion in the first half of the year, billion-dollar rounds for Hadrian, Base Power, and Valar Atomics, energy and AI chips as the new mainstream, an IPO conveyor from SpaceX to Anthropic, and the situation in the markets of Russia and the CIS.

The fuel and energy complex (FEC) starts a new week in a state of heightened uncertainty. The main topic for investors and participants in the commodity market is the fate of the Strait of Hormuz: Washington claims to be close to an agreement with Tehran, while the Iranian side denies any direct negotiations, and attacks on commercial shipping continue. Against this backdrop, Brent oil remains above $84 per barrel, and WTI approaches $79. OPEC+ has formally completed the return of voluntary production cuts; however, physical supply in the market remains limited. The European gas market enters a critical phase of injection with near twenty-year low reserves, coal prices rise amid Asian heatwaves, and renewable energy continues to set historical records. In Russia, authorities note the end of the acute phase of the fuel crisis. A detailed overview of key events in the oil, gas, and energy sector is provided below.

The fuel and energy complex (FEC) begins a new week amidst heightened uncertainty. The main topic for investors and commodity market participants is the fate of the Strait of Hormuz: Washington announces closeness to an agreement with Tehran, while the Iranian side denies any direct negotiations, and attacks on commercial shipping continue. Against this backdrop, Brent oil remains above $84 per barrel, while WTI approaches $79. OPEC+ has formally completed the return of voluntary production cuts, yet the physical supply in the market remains limited. The European gas market enters a decisive phase of injection with inventories at almost twenty-year lows, coal prices rise amid Asian heat waves, and renewable energy continues to set historical records. In Russia, authorities confirm the end of the acute phase of the fuel crisis. A detailed review of key events in the oil and gas and energy sectors is presented below.

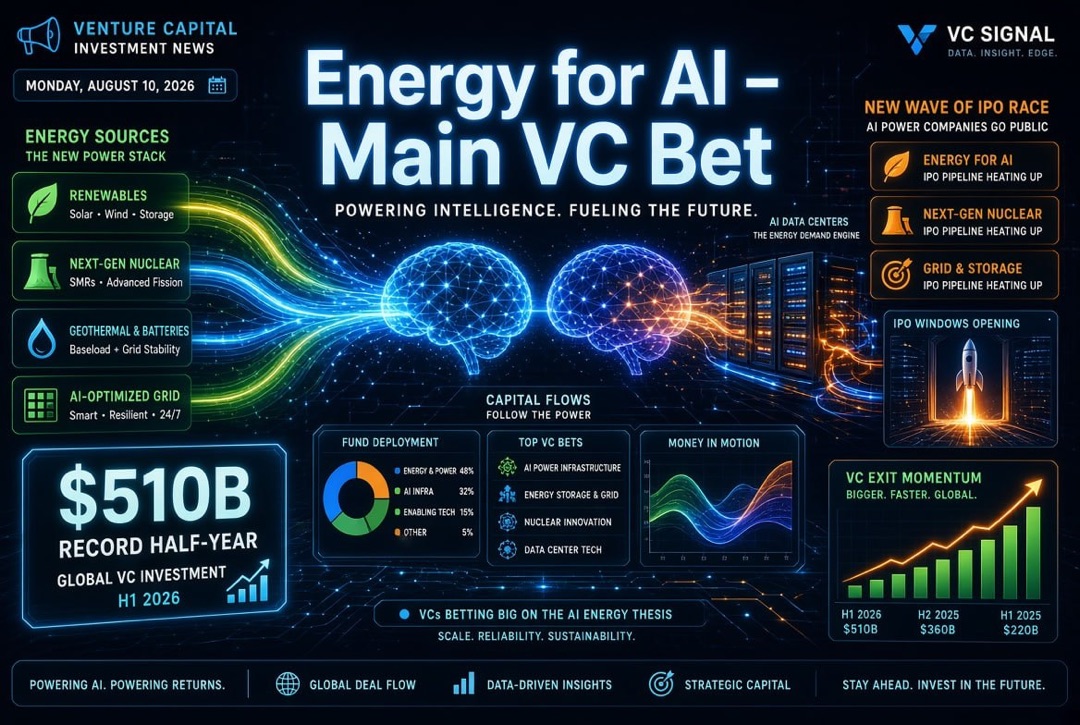

Current news on startups and venture investments as of August 10, 2026: billion-dollar rounds in energy infrastructure for artificial intelligence, record venture capital concentration, a revival in the IPO market, and key trends for venture investors and funds.

The economic events and corporate reports for Saturday, August 8, 2026, left a significant mark on the financial markets. These events, including the week’s results following the Payrolls, inflation in China, and preparations for the upcoming Consumer Price Index (CPI) release in the United States, instill certain expectations and forecasts. This week, investors closely monitored how employment changes and inflation data from China could impact global markets. The influence of these factors is becoming increasingly palpable as preparations for the next CPI report in the U.S. continue. These key elements have emerged as central themes in the economic arena, shaping the directions of the global economy in the near future. In this article, we will explore how the recent events have influenced the economic landscape and what further steps can be expected from the largest players in the financial field. Learn more about how the outcomes of the week after Payrolls and other economic data are shaping the future prospects of the global financial market.

Friday, August 7, 2026, will be a real test for the global economy. On this day, significant economic events and corporate reports are expected that could impact international markets. The focus will be on the monthly Nonfarm Payrolls release in the United States, providing insight into the state of the American labor market. China will present its trade balance data, helping to assess the economic recovery after global disruptions. Germany will release industrial production reports, offering information on the condition of one of Europe's largest economies. Equally important will be the earnings report from Allianz, which will affect not only the financial sector but also the overall understanding of the direction of European business. A detailed review of each of these events will help investors, analysts, and all stakeholders better understand current economic dynamics and make more informed decisions.

Cryptocurrency News: Friday, August 7, 2026 - a day when the cryptocurrency market is focused on an important event. The U.S. Senate is preparing to vote on the CLARITY Act, which could significantly change the game for companies and investors in the cryptocurrency world. This bill aims to provide clarity and transparency in regulation within the crypto industry, which should stimulate more active participation from large investment funds and minimize risks for retail investors. The outcome of the vote is expected to have a significant impact on the prices of major cryptocurrencies such as Bitcoin and Ethereum, determining the future trajectory of the market. Analysts warn of potential increased volatility in the coming days, creating unique opportunities for traders and investors. Only hours remain before the vote, and the market holds its breath in anticipation of this key event.

The fuel and energy complex (FEC) greets Friday, August 7, 2026, amid heightened volatility. The main driver of the week has been the negotiations between the USA, Iran, and Oman regarding the opening of the Strait of Hormuz—a key artery for the global trade of oil and liquefied natural gas (LNG). Expectations of a quick deal have plunged oil quotes by more than 5% in a single session, with Brent retreating from local highs at the end of July to about $79 per barrel. Simultaneously, OPEC+ concludes its annual production increase cycle as Europe enters the heating season with the lowest level of gas storage in five years, while Russia continues to maintain its ban on the export of petroleum products amid domestic fuel shortages. For investors, traders, and market participants, this presents a rare combination of geopolitical easing in the Middle East and a structural gas deficit in Europe—a combination that will dictate the dynamics of oil, gas, petroleum products, and electricity in the coming weeks.

On Friday, August 7, 2026, the global venture investment market continues to show remarkable resilience amid overall macroeconomic uncertainty. The key theme of the week is the rapid reallocation of capital towards AI physical infrastructure: energy, data centers, and computing power. Simultaneously, there is an accelerating flow of venture money into defense technologies, and the IPO market is gearing up for a wave of megasized placements that could be the largest in the history of the tech sector. For venture investors and fund managers, this week reinforces the main trend of the second half of 2026: capital is moving away from 'light' digital products towards capital-intensive, infrastructure bets on the future of the AI economy.